You can download the Final Accounts Format PDF for free by using the direct link provided below on the page.

Final Accounts Format PDF

The process of preparing Final Accounts involves several essential steps that are meticulously followed to ensure accuracy and completeness in financial reporting. Initially, the financial data is recorded through journal entries, where transactions are documented in chronological order to maintain a clear and organized record of all financial activities. Subsequently, the recorded data is transferred to the ledger, which acts as a central repository for all financial transactions. The ledger organizes the information into specific accounts, such as assets, liabilities, equity, revenue, and expenses, facilitating the tracking and management of financial data in a structured manner.

As the financial data is systematically recorded and organized in the ledger, the next step involves the compilation and creation of the Final Accounts. These accounts typically include the Income Statement (Profit and Loss Account), Balance Sheet, and Cash Flow Statement, each serving a distinct purpose in presenting the financial performance and position of the business. The Income Statement provides a detailed summary of the revenues earned and expenses incurred during a specific accounting period, ultimately determining the net profit or loss generated by the business. It offers valuable insights into the operational efficiency and profitability of the organization, guiding decision-making processes for future financial strategies.

On the other hand, the Balance Sheet presents a snapshot of the financial position of the business at a given point in time, showcasing the assets owned, liabilities owed, and the equity of the owners. This statement is instrumental in assessing the solvency, liquidity, and overall financial health of the organization, enabling stakeholders to make informed decisions based on the financial standing of the business. Additionally, the Cash Flow Statement outlines the inflows and outflows of cash and cash equivalents during a specific period, highlighting the sources and uses of cash within the business. This statement is essential for evaluating the cash-generating ability of the organization and ensuring sufficient liquidity to meet financial obligations and investment requirements.

The preparation of Final Accounts is a meticulous process that culminates in the creation of comprehensive financial statements, offering a detailed overview of the financial performance, position, and cash flows of a business. By following the prescribed steps and adhering to accounting principles, organizations can accurately communicate their financial status to stakeholders and make informed decisions to drive future success and growth.

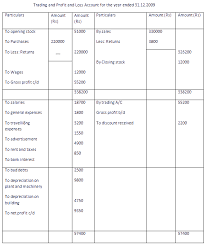

Study of Debit side of Trading Account

- Opening Stock is a crucial element in the Trading Account, representing the unsold closing stock from the previous financial year that carries over to the current financial period. This opening stock is recorded on the debit side of the Trading Account as “To Opening Stock,” providing a starting point for the inventory valuation in the new accounting cycle.

- Purchases play a significant role in the Trading Account, encompassing the total value of goods acquired during the current financial year, including both cash and credit purchases. These purchases, net of any returns, are recorded on the debit side of the Trading Account as “To Purchases,” reflecting the cost of acquiring inventory for resale or production.

- Direct Expenses are essential costs incurred in conjunction with obtaining and preparing traded goods for sale or production. These expenses, such as freight charges, cartage, custom duties, utilities, packaging materials, and wages directly related to the goods, are recorded on the debit side of the Trading Account under specific expense categories, providing a detailed breakdown of the costs associated with the traded goods.

- Sales Account represents the total revenue generated from the sale of goods, both cash and credit transactions. This sales figure is displayed on the credit side of the Trading Account as “By Sales,” showcasing the income generated from the sale of goods after deducting any applicable taxes and duties, providing a clear view of the revenue generated from the trading activities.

- Closing Stock signifies the total value of unsold inventory at the end of the current financial year, serving as a critical component in determining the cost of goods sold and the overall profitability of the business. This closing stock value is recorded on the credit side of the Trading Account, calculated as the sum of the opening stock, net purchases, and net sales, offering insights into the inventory levels and financial performance.

- Gross Profit is a key indicator of the profitability of the business, representing the difference between sales revenue and the cost of goods sold. This gross profit margin is calculated before deducting operating expenses, taxes, and other financial obligations, providing a measure of the efficiency and profitability of the core business operations.

- Operating Profit reflects the profitability of the business from its primary operations, excluding non-operating items such as interest, taxes, and investments. This operating profit margin is calculated before deducting non-recurring expenses, offering a clear view of the business’s profitability from its core activities. Operating profit is a vital metric for assessing the financial performance and sustainability of the business.